The urgency and cross-cutting nature of climate change requires an adaptation of existing public financial management (PFM) practices to ensure that climate concerns are taken into consideration at every step of fiscal and budget policies, from their design to their implementation.

In August 2021, an IMF Staff Climate Note outlined a framework (“Green PFM”) for the integration of an environment and/or climate-friendly perspective into PFM practices and processes. The Green PFM framework provides a holistic view of entry points and opportunities for integrating climate priorities into PFM frameworks. It can be applied to all countries regardless of their income level or capacity.

Building on this Staff Climate Note, a newly published How-to-Note (How to Make the Management of Public Finances Climate Sensitive) presents details of the Green PFM framework supported by a wide range of country examples. It provides operational advice to governments, including a complete picture of entry points within the budget cycle that offer opportunities for deeper integration of environmental and climate priorities. It also specifies areas of interaction with PFM functions that go beyond the scope of the budgetary cycle, such as coordination with other public sector entities or fiscal transparency.

The IMF’s Green PFM Framework relies on the following series of questions:

- Strategic Planning and Fiscal Framework—do strategic planning tools (a country’s national development plan, its medium-term fiscal framework) consider environmental / climate concerns?

- Budget Preparation—are tools in place to integrate environmental / climate concerns into the budget preparation and allocation process (e.g., climate impact assessments, tagging of expenditures affecting the environment, green spending reviews)?

- Budget Execution and Accounting—is the PFM system able to track and monitor the outcomes of “green” expenditures?

- Control and Audit – are national audit offices and other oversight institutions equipped to analyze climate-related expenditures and outcomes and hold public officials to account for the results?

- Legal Framework—are green PFM practices underpinned by an adequate legal framework?

- Public Investment Management (PIM) – do choices regarding the planning, allocation of resources, and implementation of public infrastructure investment adequately reflect climate concerns, both in terms of how countries adapt to climate change and mitigate the impact of environmental shocks?

- Fiscal Transparency – are efforts being made to ensure transparency and accountability for environmental and climate aspects of fiscal and budget policies across the PFM cycle?

- Coordination with Subnational Governments and State-owned Enterprises – have PFM practices been adjusted to ensure that these important fiscal actors play a role in the achievement of environmental goals?

Although no government has yet adopted a comprehensive “Green PFM” system, a growing number of governments are implementing good practices in one or more of the areas listed above. The How-to-Note presents country examples relevant for each key PFM area where environmental / climate concerns should be “mainstreamed”. Examples include the following:

- requiring that national and sectoral development strategies are aligned with commitments on the mitigation of and adaptation to climate change (China, South Africa);

- adopting macro-fiscal forecasting and modelling tools that incorporate climate and environmental impacts to inform the preparation of a country’s fiscal strategy and the budget (Denmark);

- providing instructions in the budget circular on how spending entities should incorporate climate-related factors in their budget submissions (Kenya);

- setting requirements for the systematic analysis of the climate impact of new fiscal measures before their adoption (Philippines) or for inclusion of climate risk in all investment projects (Peru);

- publishing ex post reviews of the climate outcomes of budget policies (Bangladesh, Italy); and

- integrating climate change considerations into ex post audit methodologies (Canada).

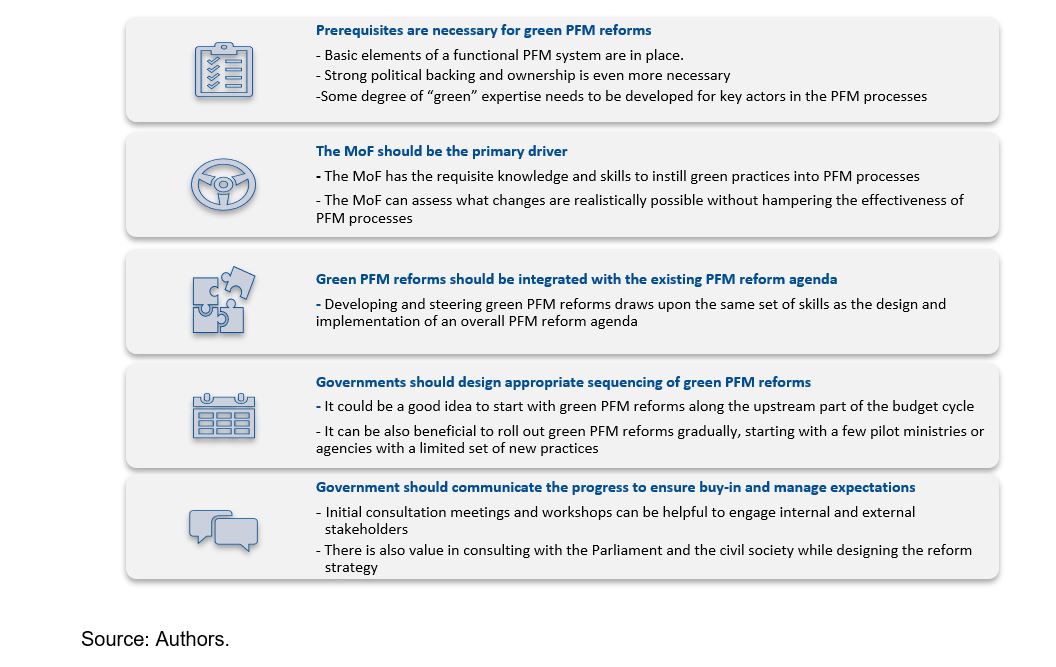

With governments showing growing interest in greening their PFM systems and practices, the How-To-Note emphasizes the importance of country-specific reform strategies consistent with each country’s legal framework, capacity levels, and reform agenda. It further details five key principles (see below) to ensure a successful implementation of green PFM reforms.

To help IMF member countries integrate environmental and climate priorities into their PFM systems, the Fund’s Fiscal Affairs Department (FAD) is providing capacity development support including through bilateral technical assistance missions and peer-learning seminars. Early examples of this support have included providing technical assistance missions to the Turks and Caicos Islands (mainstreaming green and gender budgeting processes into the budget cycle) and Serbia ("green budget tagging" and identifying PFM practices that can be enhanced to support green budgeting). FAD has also conducted regional seminars in South and Southeast Asia. An online course on Green PFM presented by the IMF's Institute for Capacity Development and FAD provides an opportunity to learn more about Green PFM.

The IMF will continue to promote its Green PFM Framework and provide capacity development support to member countries interested in greening their PFM systems, in conjunction with other tools developed by FAD (e.g., the climate module of the Public Investment Management Assessment (C-PIMA) and the Fiscal Risk Toolkit) or with other partners such as the United Nations Development Program or the World Bank, notably in the context of the efforts of the Coalition of Finance Ministers for Climate Action.