Credit micheile dot com/unsplash

Credit micheile dot com/unsplash

Spending reviews can help manage global fiscal challenges.

Credit micheile dot com/unsplash

Credit micheile dot com/unsplash

Spending reviews can help manage global fiscal challenges.

Before the COVID-19 pandemic, spending reviews were emerging as an important public financial management tool. In 2020, more than three-quarters of OECD countries reported that they conducted spending reviews either annually or periodically. As we emerge from the pandemic, and the world faces high levels of debt, hugely increased energy costs, and rising inflation, countries have a renewed interest in undertaking spending reviews. These reviews can help policymakers address ongoing fiscal challenges and reassess budget priorities. They can help meet new policy objectives such as targeting assistance to groups that may have been disproportionately affected by the pandemic or rising energy costs, such as women, low-income households and other vulnerable groups.

A new IMF report “How To Design and Institutionalize Spending Reviews” compiles advanced and emerging countries’ recent experiences with the implementation of spending reviews. It identifies key success factors and makes recommendations for conducting these reviews.

Spending reviews refer to the process of conducting in-depth assessments of existing public expenditure to identify opportunities for reducing or redirecting spending from low-priority, inefficient, or ineffective spending to higher value expenditure. They offer a systemic approach to ensuring that spending is aligned with the government’s policy priorities, is effective in achieving its intended objectives and is deployed efficiently.

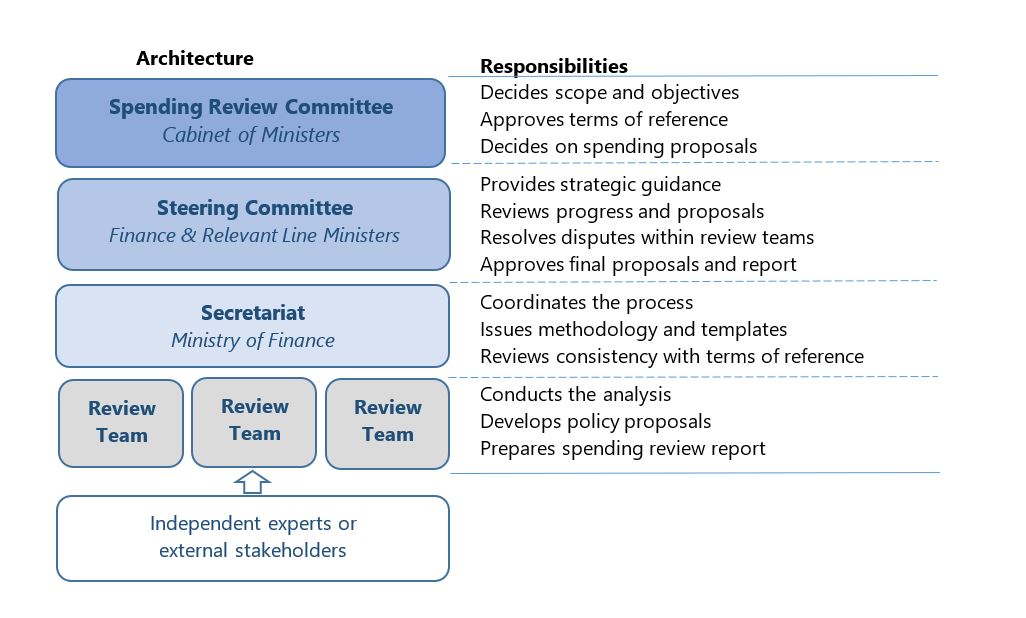

The How-to-Note recommends an organizational structure to support the spending review framework with clearly defined roles and responsibility driven by ministries of finance. Experience suggests the following organizational principles for conducting spending reviews: (i) strong oversight and coordination by the finance ministry; (ii) availability of a broad knowledge base to develop policy proposals; and (iii) a decision-making mechanism at ministerial level to ensure there is political commitment to the process across the government. (See Figure 1)

Fig.1

The How-to-Note sets out a four-stage process for conducting spending reviews. It provides guidance and examples for each stage and proposes mechanisms through which the outcomes of spending reviews can be integrated into the budget process. The four stages comprise: (1) objective setting and design; (2) identification of saving options based on in-depth analysis; (3) deciding on measures to include in the budget; and (4) implementation of the findings of the review.

A credible budget process, a medium-term budget framework, and performance information linked to the outputs and outcomes of public spending ensure that the spending review objectives are aligned with the government’s fiscal objectives and that the outcomes of the reviews can be fully integrated with budget procedures.

However, spending reviews (or some parts of a spending review framework) may still be effective in countries where the budget process is underdeveloped. For example, low-capacity countries can opt for a more streamlined process, focusing primarily on the largest areas of expenditure, examination of spending trends, areas of consistent over- or under-execution of the budget, and simplified cross-country benchmarking drawing on external information sources.

Low-capacity countries can also consider adopting elements of a spending review framework as a starting point for improving expenditure analysis. This could take the form of high-level benchmarking or the development of basic performance indicators in the largest spending areas. For example, in many lower-income countries, a large portion of the annual budget is the public sector wage bill.

The How-to-Note suggests that spending reviews are more likely to be successful if the following conditions are satisfied: