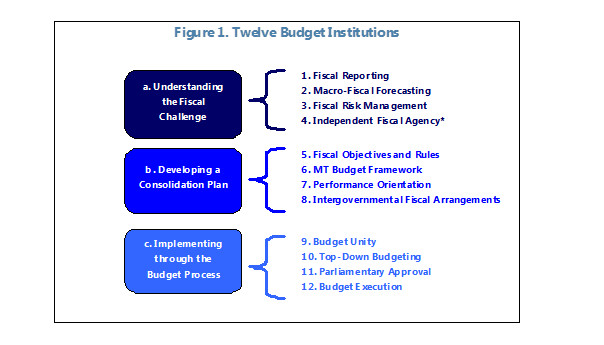

The paper identifies 12 institutions (see figure1) that the literature suggests are important for the effectiveness of fiscal policy. To be clear, the term institution is used in a broad sense—it encompasses processes, procedures, systems, legal frameworks, and organizational entities which contribute to the budget process. The institutions are separated into three groups. Those that help identify the fiscal challenges a country faces, those that help develop appropriate adjustment plans, and finally those that support implementation of any adjustment plan approved by government. For example, the fiscal reporting system can be seen as one of the important institutions for identifying the fiscal difficulties a country may face. If fiscal reports do not cover a large part of the public sector, are not timely, or there are few assurances of the integrity of the data, the fiscal reporting institution is assessed as weak. For each of the 12 institutions, a number of criteria were identified that enabled assessment of their relative strength.

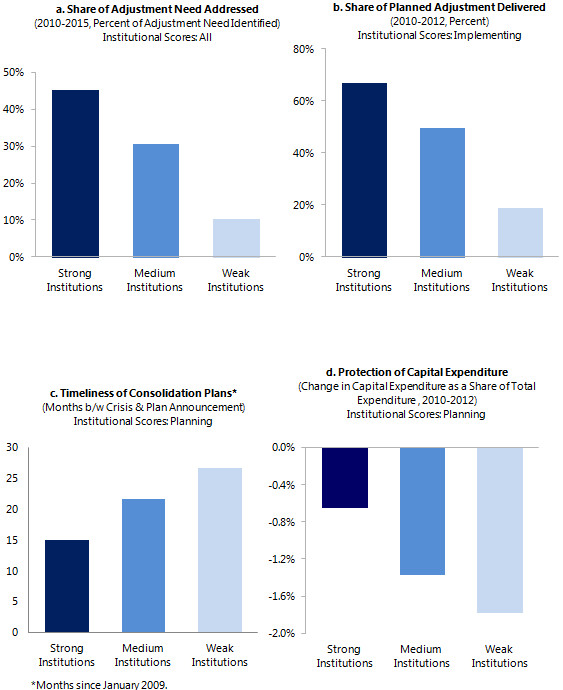

The 12 institutions were then tested, individually or in aggregate form (by the groups mentioned above, or in total), against a number of indicators of fiscal performance. The graphs below perhaps show the most interesting findings. Countries with stronger institutions overall seem to evaluate the need for adjustment more in line with what, for example, the IMF has advised that the consolidation effort should be (graph a). Countries with strong implementing institutions carry out much more of their announced adjustment plans than countries with weak institutions (graph b). Intriguing is also that countries with strong budgetary planning institutions tend to develop and announce their adjustment strategies more rapidly (graph c), and protect capital expenditure (graph d) – important for long-term growth – more successfully during consolidation.

So are there any caveats to this analysis? Yes, of course. The main ones are that the findings are based on a relatively small group of countries and that the period of investigation was quite short (2010-13). As always, proving causality is problematic in institutional analyis. The analysis is also not normative in that it does not pass judgement on whether the fiscal policy effort of countries during the period was appropriate for the stage of the economic cycle. Further analysis and confirmation of the results will be necessary in the coming years.

It is interesting to note, however, that countries themselves seem very much convinced that institutions do matter. G-20 countries are voting with their feet in pursuing reforms especially those under fiscal pressure in the wake of the crisis. Reforms have been uneven across country groupings and across institutions. Advanced G-20 economies, especially those in Europe, and those with a specific consolidation plans seemed to have been the strongest reformers. Emerging market economies, those with no specific consolidation needs, and countries with a federal government structures, seemed less inclined to reform. This has contributed to a growing gap in institutional strength between advanced and emerging G-20 countries.

Looking at the type of reforms that have been popular it is clear that independent fiscal agencies, fiscal objectives and rules and medium-term budgetary frameworks have been the flavor du jour of budget reforms since the crisis (see graph e). These reforms have been important in making economic forecasts less biased, fiscal frameworks more credible and fiscal policy more sustainable. They were also an essential part of making fiscal policy coordination possible in the Euro zone.

Reforms requiring relatively more administrative or political effort have seen less progress, both in advanced and emerging economies. Changes in fiscal reporting and fiscal risk management have been relatively limited which still makes it difficult for policy makers and politicians to fully understand the fiscal challenges they are facing. Also changes to intergovernmental financial arrangements – to better coordinate fiscal policy between layers of government – have seen few improvements. Extra-budgetary funds and other earmarks, summarized in the “budget unity” institution, still limit budget flexibility in many countries.

The report concludes with a country annex setting out priorities for further institutional reform for each of the G-20 countries. The overall message is that, over the past three years, G-20 countries have made progress in strengthening their budget institutions and that these institutions have played a critical role their adjustment strategies. However, there remains considerable scope to reinforce the institutional architecture for fiscal policymaking in all G-20 countries.

Note: The posts on the IMF PFM Blog should not be reported as representing the views of the IMF. The views expressed are those of the authors and do not necessarily represent those of the IMF or IMF policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}